Home Equity Loans: Key Comparisons

By Isabella Chalmers / Oct 23

Have you ever considered how your home can be more than just a place to live? By understanding home equity, you can unlock new financial opportunities that could transform your future!

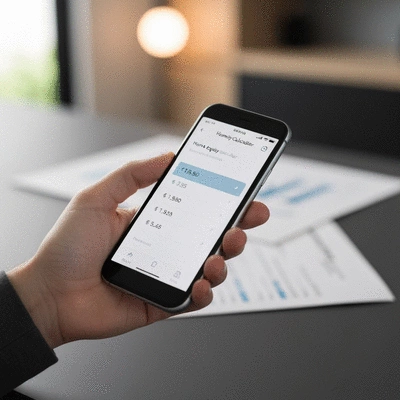

This visual details the core components and calculations essential to understanding home equity loans in Australia.

A lump sum borrowed against your property's value, secured by your home. Typically offers lower interest rates than unsecured loans.

Learn More →Formula:

Current Market Value - Outstanding Mortgage =

Home Equity

Example: $600,000 (Value) - $400,000 (Mortgage) = $200,000 (Equity)

Formula:

(Loan Amount / Property Value) × 100 =

LVR (%)

LVR below 80% is often preferred by lenders. High LVRs may require additional insurance.

When diving into the world of home financing, one question often arises: What exactly is a home equity loan? At its core, a home equity loan allows homeowners to borrow against the equity they've built in their property. This type of loan can be a valuable resource for those looking to fund renovations, consolidate debt, or even invest in new opportunities! For more detailed insights, consider reading our article on understanding home equity loans.

In Australia, these loans are typically secured by your home's value, and they can provide access to significant funds. It's crucial to understand how you can leverage this aspect of homeownership effectively. So, let’s break it down!

A home equity loan is a product that allows you to borrow a lump sum, using your property as collateral. Essentially, you’re tapping into the value of your home, which can often be a smart financial move when used responsibly. This type of loan typically has lower interest rates compared to unsecured loans, making it an attractive option for many homeowners.

Since I founded Equity Loan Hub, I’ve seen countless Australians benefit from understanding and utilizing their home equity. By accessing a home equity loan, you can turn your property’s worth into cash for your immediate needs!

Calculating home equity is fairly straightforward. You simply take the current market value of your home and subtract any outstanding mortgage balances. Here’s the formula: Home Equity = Current Market Value - Outstanding Mortgage. For example, if your home is valued at $600,000 and you owe $400,000 on your mortgage, your home equity stands at $200,000. To learn more about this, check out our guide on calculating home equity for loans.

By regularly evaluating your home’s value and mortgage balance, you can keep tabs on your equity and make informed decisions about financing. Understanding this dynamic is essential for any homeowner!

Several factors can influence your home equity calculation, including market trends, property improvements, and changes in your mortgage. For instance, if property values in your area increase, your equity could grow even without any mortgage payments being made. Similarly, investing in renovations can boost your home’s market value, further enhancing your equity.

It’s important to keep these factors in mind, especially if you’re considering a home equity loan. Responsible borrowing that aligns with the current market can make a significant difference!

The Loan-to-Value Ratio (LVR) is a crucial metric lenders use to assess risk when approving home equity loans. To determine your LVR, divide the amount you wish to borrow by your property's appraised value and multiply by 100. For example, if you want to borrow $100,000 on a home worth $500,000, your LVR would be 20%.

Keeping your LVR in check is essential when exploring your home equity options. It not only impacts your chances of approval but can also affect the interest rate you receive.

Home equity plays a vital role in property ownership, providing financial flexibility and opportunities for investment. It’s not just about the numbers; it represents the ownership you have in your home, which can be a powerful asset!

At Equity Loan Hub, we believe that understanding the significance of home equity equips homeowners to make smarter financial decisions. This equity can be used strategically to improve your financial situation and overall lifestyle.

Understanding property equity is essential for any homeowner. It’s not just about accessing funds; it’s about leveraging your home’s value to enhance your lifestyle. Whether you’re considering renovations or consolidating debt, your home equity can provide a means to achieve your goals.

By viewing your property equity as a tool rather than just an asset, you empower yourself to make decisions that can yield long-term benefits. So, take a moment to assess your equity and consider how it can work for you!

When considering a home equity loan, always aim to keep your Loan-to-Value Ratio (LVR) below 80%. This not only enhances your chances of approval but can also lead to better interest rates and lower costs over time. Regularly monitor your property’s value and your outstanding mortgage to stay on top of your equity situation!

When it comes to home equity loans, making informed decisions is crucial. After all, your home is one of your most significant assets, and using its equity wisely can open doors to financial opportunities. One way to ensure you're making the right choices is by consulting with a mortgage broker. But when should you seek their help, and why is it important?

Mortgage brokers can be invaluable resources when navigating the complexities of home equity loans. They are experts in the field who can provide personalized advice tailored to your situation. If you're feeling overwhelmed by your options or unsure about the potential implications of a loan, don't hesitate to reach out to a broker. Here’s when you might consider consulting with one:

Engaging with a mortgage broker can save you time and stress, allowing you to focus on what matters most—making the best financial choices for your future!

Another way to make informed decisions is by utilizing online tools and calculators. At Equity Loan Hub, we believe that having accurate numbers at your fingertips can empower you to take control of your financial journey. Here are some essential tools you should consider:

By leveraging these resources, you can clarify your financial standing and make more confident decisions regarding your home equity loan. For further reading, explore our guide on applying for a home equity loan.

Home loan calculators not only provide estimates on your repayments but can also help you visualize different scenarios. For example, playing around with different interest rates can show you how even a small change can impact your monthly budget! On the other hand, loan comparison websites allow you to quickly assess offers from various lenders in one place. This saves time and helps ensure you’re making the most informed choice.

Here are some common questions about home equity loans to help you further understand this financial tool.

Here is a quick recap of the important points discussed in the article:

By Isabella Chalmers / Oct 23

By Isabella Chalmers / Oct 23

By Isabella Chalmers / Oct 23