Considering a home renovation? You might find that tapping into your home's equity could be the key to unlocking the funds you need. Understanding your options between home equity loans and lines of credit can empower you to make informed financial decisions. Let’s explore the essentials!

What You Will Learn

A home equity loan provides a lump sum at a fixed interest rate, ideal for large projects with clear budgets.

A HELOC offers a revolving line of credit with variable interest rates, allowing for flexibility in ongoing renovations.

Understanding your home equity calculation is crucial; it’s the difference between your home’s market value and your remaining mortgage balance.

Different renovation types may require different financing options; choose based on whether your project is a one-time renovation or an ongoing improvement.

Be aware of the risks involved, including the possibility of foreclosure if payments are missed, especially with variable rates.

Additionally, explore grants and programs that may provide financial assistance for renovations, supplementing your financing strategy.

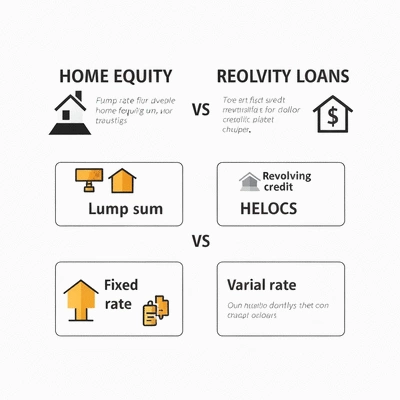

Home Equity Financing Options: Loan vs. HELOC

Understanding the key differences between a Home Equity Loan and a Home Equity Line of Credit (HELOC) is crucial for making informed decisions about financing your home renovations. This comparison highlights their distinct structures, interest rate types, and suitability for various project needs. For a deeper dive into the fundamental concepts, explore understanding home equity loans.

Home Equity Loan

Lump Sum Disbursement

Receive a single, large payment upfront.

Fixed Interest Rate

Interest rate remains constant throughout the loan term.

Predictable Repayment

Monthly payments are consistent and known in advance (5-30 years).

Ideal For:

Large, one-time projects with a clear budget.

Home Equity Line of Credit (HELOC)

Revolving Credit

Borrow funds as needed, up to a set limit, like a credit card.

Variable Interest Rate

Interest rate can fluctuate with market conditions.

Flexible Draw & Repayment

Draw period (5-10 yrs) followed by repayment, often interest-only initially.

Ideal For:

Ongoing projects with evolving costs or phased renovations.

Understanding Home Equity Financing for Renovations

As a homeowner, you might be wondering how to tap into the financial potential of your property for your next renovation project. That's where understanding home equity financing comes into play! In this section, I'll break down the concepts of home equity loans and lines of credit, giving you clarity on your options.

What is a Home Equity Loan?

A home equity loan is essentially a way to borrow against the equity you've built up in your home. Think of it as a second mortgage. This type of loan provides you with a lump sum of money that you pay back at a fixed interest rate. It's straightforward and predictable, so you know exactly what your monthly payments will be.

Lump Sum Disbursement: You receive a one-time payment, making it great for larger projects.

Fixed Interest Rates: Your interest rate remains constant throughout the loan term, which can be comforting in a fluctuating market.

Repayment Terms: Typically ranges from 5 to 30 years, allowing for flexible repayment options.

It's a solid choice if you have a specific renovation in mind and need a clear budget. However, make sure your renovation project aligns with your financial goals!

What is a Home Equity Line of Credit (HELOC)?

On the other hand, a Home Equity Line of Credit (HELOC) offers more flexibility. It's structured like a credit card, allowing you to borrow money as needed, up to a certain limit. This is especially useful for ongoing projects where costs might vary.

Revolving Credit: You can borrow, pay, and borrow again, making it ideal for continuous renovations.

Variable Interest Rates: Your interest rate may fluctuate based on the market, which can be both an advantage and a risk.

Draw Period: Often, there's a draw period of 5 to 10 years where you can withdraw funds, followed by a repayment period.

This option is perfect if you’re working on phased renovations or if you anticipate unexpected expenses along the way. Just remember that managing a HELOC requires discipline to avoid overspending.

How to Calculate Home Equity for Renovations

To get started with either option, you'll need to calculate your home equity, which is crucial for determining how much you can borrow for renovations. Simply put, your home equity is the difference between your home’s current market value and any outstanding mortgage debt. Here’s how to calculate it:

Determine Your Home's Market Value: You can get this from a real estate agent, an online estimator, or a professional appraisal.

Subtract Your Mortgage Balance: Look at your current mortgage statement to find out what you owe.

Calculate Your Equity: For example, if your home is worth $500,000 and you owe $300,000, your equity is $200,000!

Understanding your home equity not only informs your borrowing limits for financing renovations but also helps you make informed financial decisions. Knowing how much you can access is vital for planning your dream renovation!

Comparing Home Equity Loans and HELOCs

Now that we've covered the basics of home equity loans and HELOCs, it's time to compare these two options. This comparison can help you decide which route is best for your renovation needs.

Key Differences in Structure and Terms

When weighing your choices, consider the following structural and term differences:

Lump Sum vs. Revolving Credit: Home equity loans provide a single disbursement, while HELOCs allow for ongoing borrowing.

Fixed vs. Variable Interest Rates: Home equity loans offer fixed rates, making budgeting easier, whereas HELOCs have variable rates that can change.

Repayment Terms: Home equity loans typically have longer repayment terms compared to the flexible structure of a HELOC.

Understanding these differences is key to aligning your choice with your renovation strategy!

Suitability for Different Renovation Types

Consider what type of renovation you're planning when choosing between a home equity loan and a HELOC. Here's a quick guide:

One-Time Large Projects: A home equity loan may be more suitable for significant renovations where you have a clear budget.

Ongoing Renovations: If your renovation plans evolve over time, a HELOC can provide the necessary flexibility.

Matching your financing option to your renovation roadmap can lead to a smoother process overall.

Understanding Risks and Considerations

As with any financial decision, it's important to understand the risks of home equity borrowing. Here are some key considerations:

Collateral Implications: Your home is the collateral for your loan, so failure to make payments can lead to foreclosure.

Payment Obligations: Ensure you can comfortably meet your repayment obligations, especially with variable interest rates in a HELOC.

Being informed about these risks helps you navigate the borrowing landscape with confidence!

Loan Comparison: Home Equity vs. Other Financing Options

Finally, let's compare home equity loans and HELOCs with other financing options:

Cash-Out Refinance: This option replaces your existing mortgage with a larger one, allowing you to access cash.

Personal Loans: Unsecured loans that can be used for renovations but often come with higher interest rates.

Credit Cards: Convenient for smaller purchases but can lead to high-interest debt if not managed properly.

Each option has its pros and cons, so consider your unique circumstances when deciding the best path for your renovation financing.

Pro Tip

When considering using home equity for your renovations, always factor in potential increases in property value. A well-planned renovation can significantly enhance your home's market value, leading to greater equity in the long run. Before committing, research current market trends and consult with real estate professionals to ensure your investment aligns with future growth.

Summarizing Key Insights for Home Renovation Financing

When considering financing for your home renovations, it's crucial to recap the main differences between a home equity loan and a Home Equity Line of Credit (HELOC). Each option has unique benefits and considerations that align with various renovation goals.

A home equity loan provides a lump sum with fixed interest rates, ideal for large, one-time projects. Conversely, a HELOC offers revolving credit with variable rates, suitable for ongoing renovations. The choice between the two largely depends on your specific needs and how you plan to manage your renovation costs.

Which Financing Option Aligns with Your Renovation Goals?

Home Equity Loan: Best for significant renovations or projects with a defined budget.

HELOC: Ideal for smaller or multiple projects, allowing flexibility in borrowing.

Interest Rates: Fixed rates for home equity loans provide stability, whereas variable rates in HELOCs can fluctuate.

Repayment Terms: Consider repayment flexibility; HELOCs often allow interest-only payments during the draw period.

Ultimately, aligning your financing option with your specific renovation goals can simplify the decision-making process. At Equity Loan Hub, we encourage you to take the time to assess what you want to achieve with your renovations!

Next Steps for Homeowners Seeking Renovation Financing

Ready to move forward? The next steps are pivotal in ensuring you select the right financing for your renovation projects. Start by evaluating your renovation needs—what do you want to change or improve in your home?

Assess Financial Situation: Check your budget and determine how much you can comfortably borrow.

Consult with Lenders: Speak to multiple lenders to compare offers and get a clearer picture of what's available.

Understand Terms: Read through loan terms carefully to avoid any surprises later on.

Consider Professional Advice: At Equity Loan Hub, we’re here to help you navigate this process!

Taking these steps will empower you to make informed decisions about your financing options for renovations, keeping your goals in sight.

Exploring Home Renovation Grants and Financial Assistance

In addition to home equity loans and HELOCs, you might want to explore various grants and financial assistance options available for home renovations. These can provide vital support, especially for specific improvement projects.

Government Grants: Look for federal or state grants designed to enhance energy efficiency or support first-time homebuyers.

Local Programs: Many local councils offer grants or low-interest loans for renovations that improve community housing.

Non-Profit Organizations: Some NGOs provide financial assistance for particular renovation needs, such as accessibility upgrades.

Exploring these options can supplement your financing strategy and potentially reduce out-of-pocket costs. Remember, being informed is key! Reach out to us at Equity Loan Hub for more insights and resources tailored to your renovation financing journey. For more detailed information on managing your finances as a homeowner, consider reading about financial tips for homeowners.

Recap of Key Points

Here is a quick recap of the important points discussed in the article:

Home Equity Loan: A lump sum loan with fixed interest rates, ideal for large, one-time renovation projects.

HELOC: A flexible line of credit that allows you to borrow as needed, suitable for ongoing renovations with variable interest rates.

Calculating Home Equity: Your equity is determined by subtracting your mortgage balance from your home’s market value.

Considerations: Understand the risks and repayment obligations, as your home is collateral for these loans.

Comparing Options: Evaluate different financing options, including cash-out refinancing and personal loans, alongside home equity solutions.

Next Steps: Assess your financial situation and consult with lenders to choose the best financing for your renovation needs.

Frequently Asked Questions About Home Renovation Financing

What is the main difference between a Home Equity Loan and a HELOC?

A Home Equity Loan provides a lump sum with a fixed interest rate, ideal for large, one-time projects. A HELOC offers a revolving line of credit with a variable interest rate, suitable for ongoing or phased renovations.

How do I calculate my home equity?

Your home equity is calculated by subtracting your outstanding mortgage balance from your home's current market value. For example, if your home is worth $500,000 and you owe $300,000, your equity is $200,000.

What are the risks associated with using home equity for renovations?

The primary risk is that your home serves as collateral. Failure to make payments can lead to foreclosure. Additionally, HELOCs have variable interest rates, which can fluctuate and potentially increase your monthly payments.

Is a home equity loan suitable for all types of renovations?

A home equity loan is best for large, one-time renovation projects with a clear and defined budget, where you need a significant amount of money upfront.

Are there other financing options besides home equity loans and HELOCs?

Yes, other options include cash-out refinancing, personal loans, and credit cards. Each has its own advantages and disadvantages regarding interest rates, repayment terms, and suitability for different project sizes.

Can I get financial assistance or grants for home renovations?

Yes, various government grants, local programs, and non-profit organizations offer financial assistance for specific types of home improvements, such as energy efficiency upgrades or accessibility modifications. It's worth exploring these to supplement your financing strategy.